Stamford, CT -

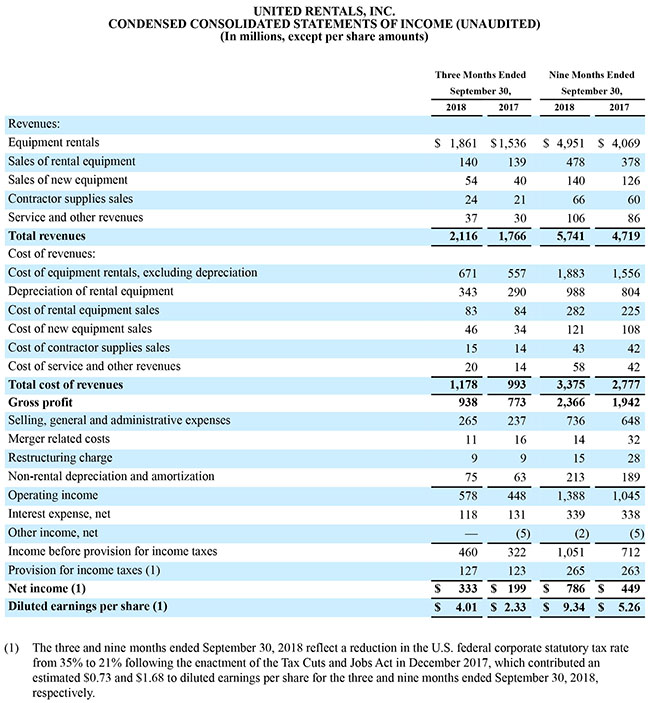

United Rentals, Inc. (NYSE : URI) a annoncé aujourd’hui ses résultats financiers pour le troisième trimestre 20181. Le chiffre d’affaires total s’élevait à 2,116 milliards USD et le chiffre d’affaires des locations s’élevait à 1,861 milliard USD pour le troisième trimestre, contre 1,766 milliard USD et 1,536 milliard USD, respectivement, pour la même période l’an dernier. Sur une base PCGR, la société a déclaré un revenu net de 333 millions USD, soit 4,01 USD par action diluée, contre 199 millions USD, soit 2,33 USD par action diluée, pour la même période l’année dernière. Le troisième trimestre 2018 comprend un avantage en matière de revenu net associé à la Loi sur les réductions fiscales et les emplois (la « Loi fiscale ») qui a été promulguée en décembre 2017. La Loi fiscale a réduit le taux d’imposition légal des sociétés fédérales des États-Unis de 35 % à 21 %, ce qui a contribué environ 0,73 USD au bénéfice par action diluée pour le troisième trimestre 20182.

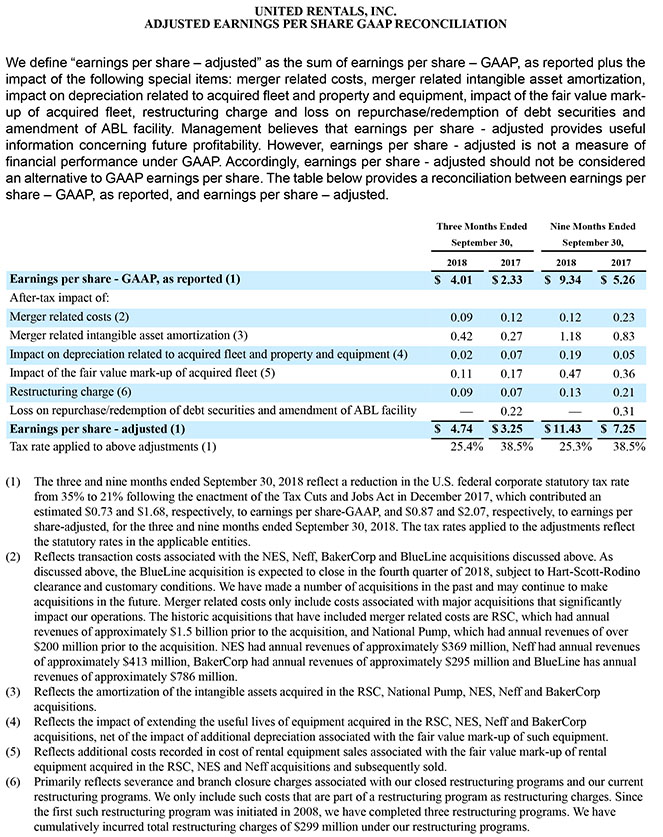

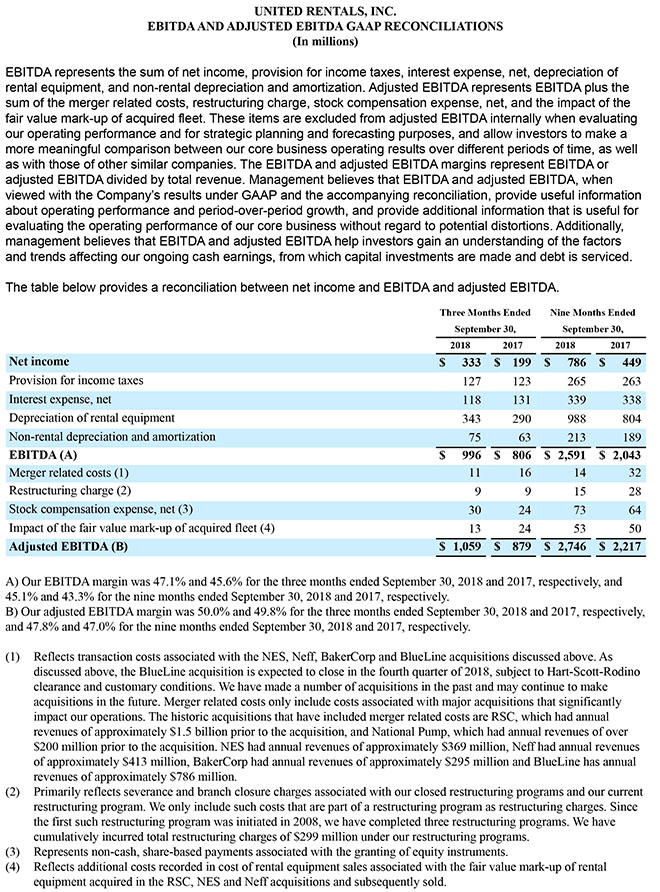

Le EPS33 ajusté pour le trimestre était de 4,74 USD par action diluée, contre 3,25 USD par action diluée pour la même période l’an dernier. La réduction du taux d’imposition discuté ci-dessus a contribué à hauteur de 0,87 USD au BPA ajusté pour le troisième trimestre 20182. L’EBITDA3 s’élevait à 1,059 milliard USD et la marge d’BAIIA ajusté3 était de 50,0 %, reflétant des augmentations de 180 millions USD et de 20 points de base, respectivement, par rapport à la même période l’an dernier. À l’exclusion de l’impact de l’acquisition de BakerCorp, la marge ajustée de l’BAIIA s’est améliorée de 80 points de base en glissement annuel pour atteindre un record de 50,6 %.

Faits saillants du troisième trimestre 2018

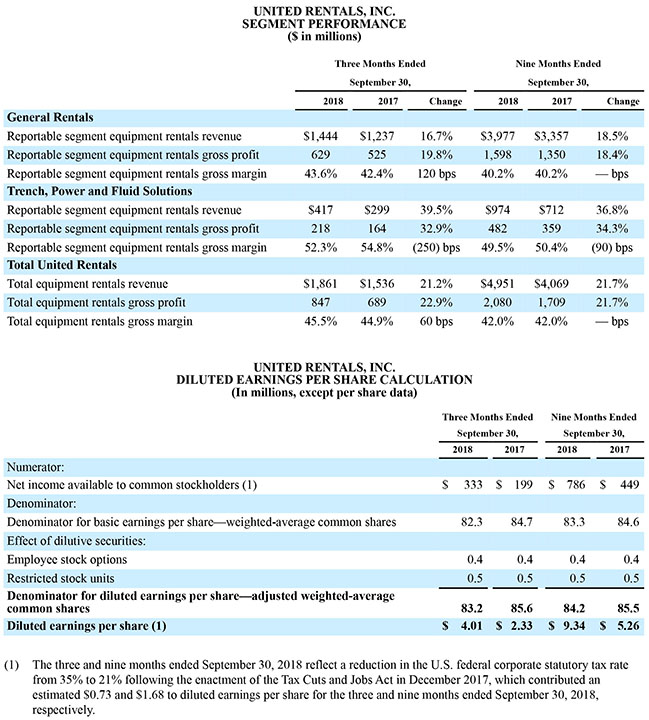

- Le chiffre d’affaires des locations4 a augmenté de 21,2 % en glissement annuel. Le chiffre d’affaires de location d’équipement détenu a augmenté de 20,3 %, reflétant des augmentations de 17,8 % du volume d’équipement en location et de 2,1 % des taux de location.

- Le chiffre d’affaires de location pro forma1 a augmenté de 10,9 % en glissement annuel, reflétant une croissance de 7,4 % du volume d’équipement en location et une augmentation de 2,1 % des taux de location.

- L’utilisation du temps a diminué de 100 points de base en glissement annuel à 70,9 %, reflétant principalement l’impact des acquisitions de Neff et BakerCorp. Sur une base pro forma, l’utilisation du temps a diminué de 10 points de base en glissement annuel à 70,7 %.

- Pour le segment spécialisé de l’entreprise, Tranches, Solutions électriques et de fluides, le chiffre d’affaires de location a augmenté de 39,5 % en glissement annuel, y compris une augmentation de 12,7 % sur la même base de magasin. La marge brute de location a diminué de 250 points de base à 52,3 %. La baisse de la marge brute de location était principalement due à l’impact de l’acquisition de BakerCorp et à une augmentation des revenus de carburant à marge inférieure, principalement dans la région Électricité et CVC1.

_______________

- L’entreprise a finalisé les acquisitions de NES Rentals Holdings II, Inc. (« NES »), Neff Corporation (« Neff ») et BakerCorp International Holdings, Inc. (« BakerCorp ») en avril 2017, octobre 2017 et juillet 2018, respectivement. Les acquisitions sont incluses dans les résultats de l’entreprise après les dates d’acquisition. Les résultats pro forma reflètent la combinaison de United Rentals, NES, Neff et BakerCorp pour toutes les périodes présentées. Les emplacements BakerCorp acquis sont reflétés dans le segment spécialisé des solutions de tranchée, d’électricité et de fluides. Le nom du segment spécialisé a été modifié (anciennement « Tranche, électricité et pompe ») pour refléter l’offre de produits plus large suite à l’acquisition de BakerCorp.

- La contribution estimée de la Loi fiscale a été calculée en appliquant la réduction du taux d’imposition en points de pourcentage au revenu avant impôt américain et les ajustements avant impôt reflétés dans le BPA ajusté.

- Le BPA ajusté (bénéfices par action) et l’BAIIA ajusté (bénéfices avant intérêts, impôts, dépréciation et amortissement) sont des mesures non PCGR qui excluent l’impact des éléments indiqués dans les tableaux ci-dessous. Consultez les tableaux ci-dessous pour connaître les montants et les rapprochements avec les mesures PCGR les plus comparables. La marge du BAIIA ajusté représente le BAIIA ajusté divisé par le chiffre d’affaires total.

- Les revenus de location comprennent les revenus de location d’équipement détenus, les revenus de location renouvelée et les revenus auxiliaires.

- L’entreprise a généré 140 millions de dollars de produits provenant des ventes d’équipement d’occasion à une marge brute PCGR de 40,7 % et une marge brute ajustée de 50,0 %, contre 139 millions de dollars à une marge brute PCGR de 39,6 % et une marge brute ajustée de 56,8 % pour la même période l’année dernière. La baisse d’une année sur l’autre de la marge brute ajustée était principalement due à l’impact de la vente de flottes plus entièrement amorties acquises dans l’acquisition de NES au troisième trimestre 20175.

Acquisition BlueLine

Le 10 septembre, 2018, la société a annoncé avoir conclu un accord définitif pour acquérir Vander Holding Corporation et ses filiales (« BlueLine ») pour environ 2,1 milliards de dollars en espèces. L’entreprise prévoit de financer l’acquisition en utilisant une nouvelle facilité de prêt à terme d’un milliard de dollars et d’autres émissions de dette. BlueLine est l’une des dix plus grandes entreprises de location d’équipement en Amérique du Nord, dessert plus de 50 000 clients dans les secteurs de la construction et de l’industrie, et compte 114 emplacements et plus de 1 700 employés basés dans 25 États américains, au Canada et à Porto Rico. BlueLine a un chiffre d’affaires annuel d’environ 786 millions de dollars. La transaction devrait être conclue au quatrième trimestre, sous réserve de l’autorisation de Hart-Scott-Rodino et d’autres conditions habituelles.

Commentaires du directeur général

Michael Kneeland, directeur général de United Rentals, a déclaré : « Nous sommes satisfaits de la force de nos résultats du troisième trimestre, y compris l’accélération de la croissance du volume et l’amélioration des marges. Nos taux étaient à nouveau positifs pour chaque mois sur un marché concurrentiel, tandis que l’utilisation du temps est restée robuste. Nous continuons à faire de bons progrès en intégrant Baker à nos opérations spécialisées, et nous sommes impatients de commencer ce processus avec BlueLine ce trimestre. »

Kneeland a poursuivi : « Nos directives actualisées reflètent la combinaison d’une forte demande du marché et des contributions de nos acquisitions terminées, qui, avec des indicateurs internes et externes, indiquent un solide quatrième trimestre et une dynamique saine en 2019. Notre stratégie reste très axée sur la croissance rentable de nos activités principales, l’intégration de nos récentes acquisitions et l’exploitation de nos flux de trésorerie pour maximiser la valeur pour les actionnaires. »

Faits saillants Neuf mois 2018

- Le chiffre d’affaires des locations a augmenté de 21,7 % en glissement annuel. Le chiffre d’affaires de location d’équipement détenu a augmenté de 21,4 %, reflétant des augmentations de 19,6 % du volume d’équipement en location et de 2,3 % des taux de location.

- Le chiffre d’affaires de location pro forma a augmenté de 11,0 % en glissement annuel, reflétant une croissance de 7,3 % du volume d’équipement en location et une augmentation de 2,4 % des taux de location.

- L’utilisation du temps a diminué de 80 points de base en glissement annuel à 68,5 %, reflétant principalement l’impact des acquisitions de NES, Neff et BakerCorp. Sur une base pro forma, l’utilisation du temps a augmenté de 20 points de base en glissement annuel à 68,2 %.

- Pour le segment spécialisé de l’entreprise, Tranches, Solutions électriques et de fluides, le chiffre d’affaires de location a augmenté de 36,8 % en glissement annuel, y compris une augmentation de 19,1 % sur la même base de magasin. La marge brute de location a diminué de 90 points de base à 49,5 %. La baisse de la marge brute de location était principalement due à l’impact de l’acquisition de BakerCorp.

- L’entreprise a généré 478 millions de dollars de produits provenant des ventes d’équipement d’occasion à une marge brute PCGR de 41,0 % et une marge brute ajustée de 52,1 %, contre 378 millions de dollars à une marge brute PCGR de 40,5 % et une marge brute ajustée de 53,7 % pour la même période l’année dernière. L’augmentation d’une année sur l’autre des ventes d’équipement d’occasion reflète principalement une augmentation du volume, entraînée par une flotte beaucoup plus grande, sur un marché solide d’équipement d’occasion.5

_______________

- La marge brute ajustée des ventes d’équipement d’occasion exclut l’impact de la majoration de la juste valeur du parc RSC, NES et Neff acquis qui a été vendu. En 2018, nous avons adopté la codification des normes comptables (« ASC »), sujet 606, « Recettes provenant des contrats avec les clients ». Les ventes d’équipement d’occasion au cours du troisième trimestre 2017 auraient été réduites de 14 millions USD en vertu du Sujet 606, car ces ventes auraient été comptabilisées avant le troisième trimestre. Le montant des ventes d’équipement d’occasion comptabilisées pour les neuf mois clos le 30 septembre 2017 ne diffère pas sensiblement du montant qui aurait été comptabilisé en vertu du Sujet 606. Bien que l’adoption du Sujet 606 ait eu un impact sur le calendrier de comptabilisation des revenus, elle n’a aucun impact sur les revenus annuels.

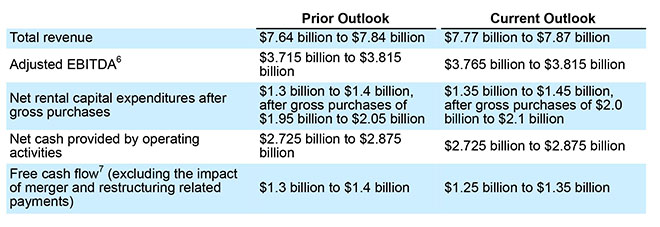

Perspectives 2018

Les directives révisées suivantes pour l’exercice complet n’incluent pas l’impact de l’acquisition imminente de BlueLine. Pour plus de détails sur BlueLine, veuillez consulter la section ci-dessus, ainsi que les présentations des investisseurs qui sont actuellement accessibles sur www.unitedrentals.com

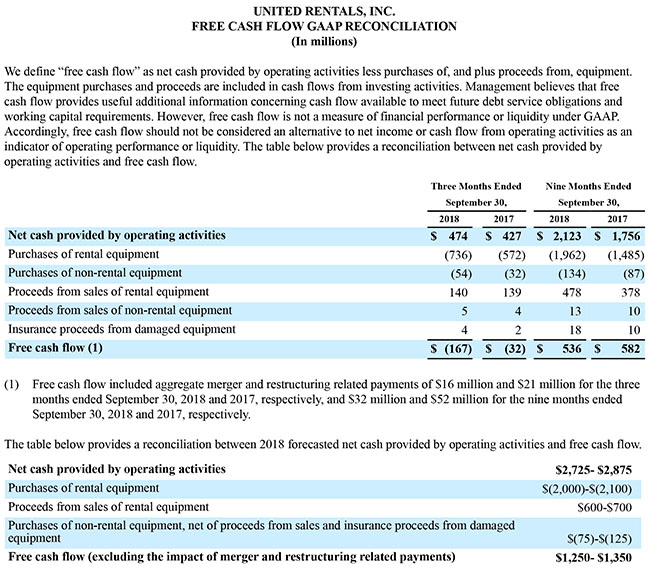

Flux de trésorerie disponible et taille du parc

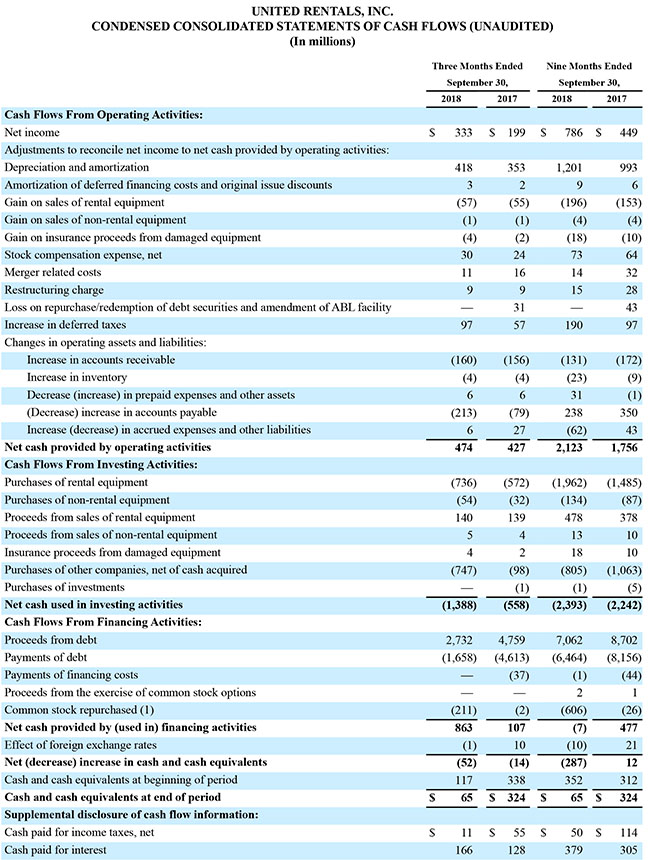

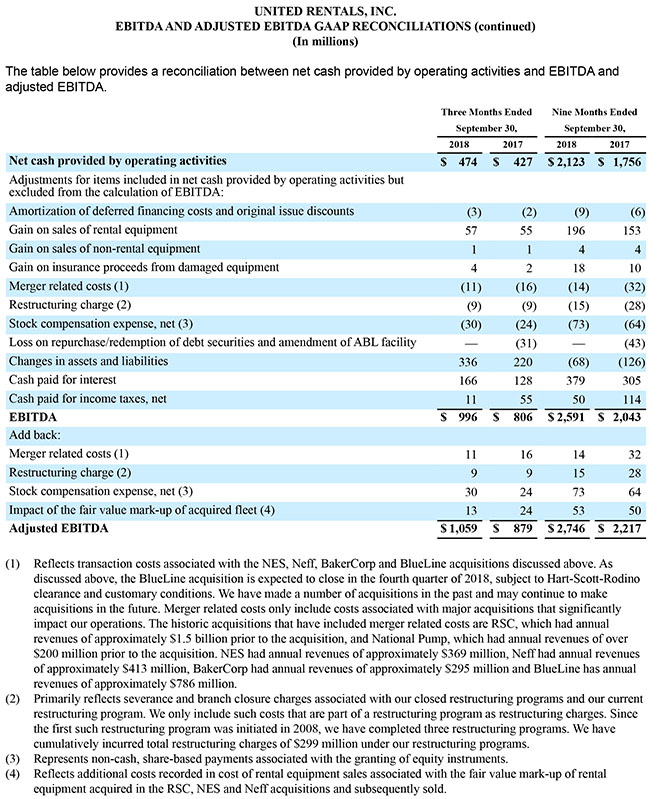

Pour les neuf premiers mois de 2018, la trésorerie nette fournie par les activités d’exploitation s’élevait à 2,123 milliards USD, et le flux de trésorerie disponible s’élevait à 536 millions USD après des dépenses d’investissement brutes totales de location et non-location de 2,096 milliards USD. Pour les neuf premiers mois de 2017, la trésorerie nette fournie par les activités d’exploitation était de 1,756 milliard USD, et le flux de trésorerie disponible était de 582 millions USD après des dépenses d’investissement brutes totales de location et non-location de 1,572 milliard USD. Le flux de trésorerie disponible pour les neuf premiers mois de 2018 et 2017 comprenait des paiements agrégés liés à la fusion et à la restructuration de 32 millions USD et de 52 millions USD, respectivement.

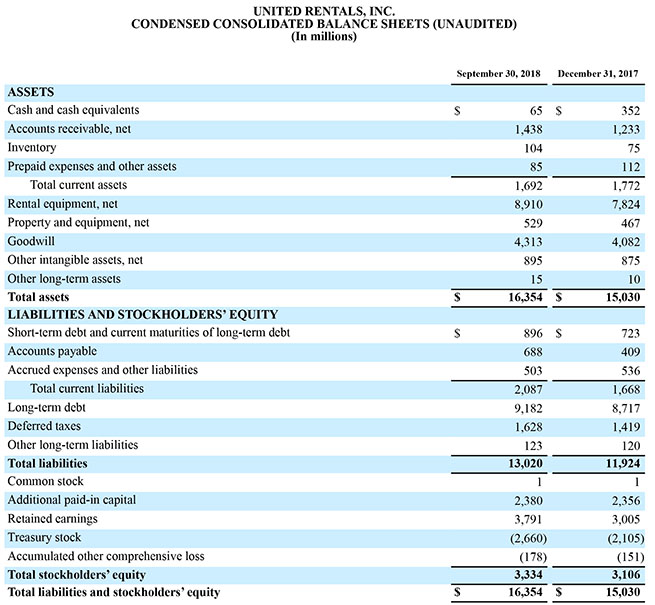

La taille du parc de location était de 12,90 milliards USD d’OEC au 30 septembre 2018, contre 11,51 milliards USD à 31 décembre, 2017. L’âge de la flotte de location était de 46,6 mois sur une base pondérée par l’OEC au 30 septembre 2018, contre 47,0 mois chez 31 décembre, 2017.

Retour sur capital investi (ROIC)

Le ROIC était de 10,7 % pour la période de 12 mois terminée le 30 septembre 2018, contre 8,6 % pour la période de 12 mois terminée le 30 septembre 2017. L’indicateur ROIC de l’entreprise utilise le bénéfice d’exploitation après impôt pour les 12 derniers mois divisé par les capitaux propres moyens des actionnaires, la dette et les impôts différés, nets de trésorerie moyenne. Pour atténuer la volatilité liée aux fluctuations du taux d’imposition de l’entreprise d’une période à l’autre, les taux d’imposition statutaires fédéraux des États-Unis de 21 % et 35 % pour 2018 et 2017, respectivement, ont été utilisés pour calculer le revenu d’exploitation après impôt.

L’entreprise s’attend à ce que le RCI augmente matériellement en raison des taux d’imposition réduits suite à l’adoption de la Loi fiscale, mais, étant donné que les 12 mois suivants sont utilisés pour le calcul du RCI, l’impact complet ne sera pas reflété avant un an après l’entrée en vigueur du taux d’imposition inférieur. Si le taux d’imposition légal de 21 % du gouvernement fédéral des États-Unis suite à l’adoption de la Loi fiscale était appliqué au RCI pour toutes les périodes historiques, la société estime que le RCI aurait été de 11,0 % et 10,3 % pour les 12 mois clos les 30 septembre 2018 et 2017, respectivement.

_______________

- Les informations qui rapprochent l’BAIIA ajusté prospectif des mesures financières PCGR comparables ne sont pas disponibles pour l’entreprise sans effort déraisonnable, comme indiqué ci-dessous.

- Le flux de trésorerie disponible est une mesure non PCGR. Consultez le tableau ci-dessous pour connaître les montants et un rapprochement avec la mesure PCGR la plus comparable.

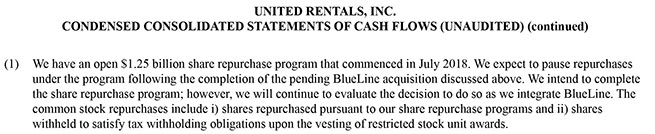

Programme de rachat d’actions

En juillet 2018, l’entreprise a commencé son programme de rachat d’actions de 1,25 milliard USD annoncé précédemment. Au 30 septembre 2018, l’entreprise a racheté 210 millions USD d’actions ordinaires dans le cadre du programme. L’entreprise s’attend à suspendre les rachats dans le cadre du programme après la finalisation de l’acquisition en cours de BlueLine mentionnée ci-dessus. L’entreprise a l’intention de terminer le programme de rachat d’actions; cependant, elle continuera d’évaluer sa décision de le faire, car elle intègre BlueLine.

Appel conférence

United Rentals tiendra une conférence téléphonique demain, jeudi 18 octobre 2018, à 11 h, heure de l’Est. Le numéro de la conférence téléphonique est le 855-458-4217 (international : 574-990-3618). La conférence téléphonique sera également disponible en direct par webémission audio à l’adresse unitedrentals.com, où elle sera archivée jusqu’au prochain appel sur les revenus. Le numéro de relecture de l’appel est le 404-537-3406, le code d’accès est le 3484139.

Mesures non PCGR

Le flux de trésorerie disponible, le bénéfice avant intérêts, les impôts, l’amortissement (BAIIABAIIA ajusté et le bénéfice ajusté par action (BPA ajusté) sont des mesures financières non PCGR telles que définies par les règles de la SEC. Le flux de trésorerie disponible représente la trésorerie nette fournie par les activités d’exploitation, moins les achats d’équipement et plus les revenus provenant de l’équipement. Les achats d’équipement et le produit représentent les flux de trésorerie des activités d’investissement. L’BAIIA représente la somme du revenu net, de la provision pour impôts sur le revenu, des intérêts débiteurs, de l’amortissement net de l’équipement en location et de l’amortissement non lié à la location. L’BAIIA ajusté représente l’BAIIA plus la somme des coûts liés à la fusion, des frais de restructuration, des dépenses de rémunération en actions, du net et de l’impact de la marge de juste valeur du parc acquis. Le BPA ajusté représente le BPA plus la somme des coûts liés à la fusion, les frais de restructuration, l’impact sur l’amortissement lié à la flotte et aux biens et équipements acquis, l’impact de la majoration de la juste valeur de la flotte acquise, la perte sur le rachat/rachat des titres de créance et la modification de la facilité d’ABL, et l’amortissement des actifs incorporels liés à la fusion. L’entreprise croit que : (i) le flux de trésorerie disponible fournit des renseignements supplémentaires utiles sur le flux de trésorerie disponible pour répondre aux obligations futures de service de la dette et aux exigences de fonds de roulement; (ii) L’BAIIA et l’BAIIA ajusté fournissent des informations utiles sur la performance opérationnelle et la croissance d’une période à l’autre, et aider les investisseurs à mieux comprendre les facteurs et les tendances qui affectent nos revenus en espèces continus, à partir duquel les investissements en capital sont effectués et la dette est traitée; et (iii) le BPA ajusté fournit des renseignements utiles concernant la rentabilité future. Cependant, aucune de ces mesures ne doit être considérée comme une alternative au revenu net, aux flux de trésorerie provenant des activités d’exploitation ou aux bénéfices par action en vertu des PCGR comme des indicateurs de performance opérationnelle ou de liquidité.

Les informations conciliant l’BAIIA ajusté prospectif avec les mesures financières PCGR ne sont pas disponibles pour l’entreprise sans effort déraisonnable. L’entreprise n’est pas en mesure de fournir des rapprochements entre l’BAIIA ajusté et les mesures financières PCGR, car certains éléments requis pour ces rapprochements sont hors du contrôle de l’entreprise et/ou ne peuvent pas être raisonnablement prévus, comme la provision pour les impôts sur le revenu. La préparation de ces rapprochements nécessiterait un bilan prévisionnel, un état des revenus et un état des flux de trésorerie, préparés conformément aux PCGR, et ces états financiers prévisionnels ne sont pas disponibles pour la société sans effort déraisonnable. L’entreprise fournit une plage pour ses prévisions d’BAIIA ajusté qui, selon elle, seront atteintes, mais elle ne peut pas prédire avec précision toutes les composantes du calcul de l’BAIIA ajusté. L’entreprise fournit une prévision de BAIIA ajustée parce qu’elle croit que l’BAIIA ajusté, lorsqu’il est vu avec les résultats de l’entreprise en vertu des PCGR, fournit des informations utiles pour les raisons susmentionnées. Cependant, l’BAIIA ajusté n’est pas une mesure de la performance financière ou de la liquidité en vertu des PCGR et, par conséquent, ne doit pas être considéré comme une alternative au revenu net ou au flux de trésorerie des activités d’exploitation comme un indicateur de la performance opérationnelle ou de la liquidité.

À propos de United Rentals

United Rentals, Inc. est la plus importante entreprise de location d’équipement au monde. L’entreprise dispose d’un réseau intégré de 1 075 succursales de location en Amérique du Nord et de 11 en Europe. En Amérique du Nord, l’entreprise est implantée dans 49 États américains et dans toutes les provinces canadiennes. Les quelque 16 700 employés de l’entreprise servent les clients de la construction et de l’industrie, les services publics, les municipalités, les propriétaires et autres. L’entreprise propose environ 3 800 catégories d’équipement à louer pour un coût d’origine total de 12,90 milliards de dollars. United Rentals est un membre de l’indice Standard & Poor’s 500, de l’indice de confiance Barron 400 et du Russel 3000 Index®, et est basé à Stamford, Conn. Vous trouverez d’autres renseignements sur United Rentals sur le site unitedrentals.com.

Énoncés prospectifs

This press release contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, known as the PSLRA. These statements can generally be identified by the use of forward-looking terminology such as “believe,” “expect,” “may,” “will,” “should,” “seek,” “on-track,” “plan,” “project,” “forecast,” “intend” or “anticipate,” or the negative thereof or comparable terminology, or by discussions of vision, strategy or outlook. These statements are based on current plans, estimates and projections, and, therefore, you should not place undue reliance on them. No forward-looking statement can be guaranteed, and actual results may differ materially from those projected. Factors that could cause actual results to differ materially from those projected include, but are not limited to, the following: (1) the challenges associated with past or future acquisitions, including NES, Neff, BakerCorp and the proposed BlueLine acquisition, such as undiscovered liabilities, costs, integration issues and/or the inability to achieve the cost and revenue synergies expected; (2) the risk that the proposed BlueLine acquisition may not be completed; (3) a slowdown in North American construction and industrial activities, which could reduce our revenues and profitability; (4) our significant indebtedness, which requires us to use a substantial portion of our cash flow for debt service and can constrain our flexibility in responding to unanticipated or adverse business conditions; (5) the inability to refinance our indebtedness at terms that are favorable to us, or at all; (6) the incurrence of additional debt, which could exacerbate the risks associated with our current level of indebtedness; (7) noncompliance with covenants in our debt agreements, which could result in termination of our credit facilities and acceleration of outstanding borrowings; (8) restrictive covenants and amount of borrowings permitted under our debt agreements, which could limit our financial and operational flexibility; (9) an overcapacity of fleet in the equipment rental industry; (10) a decrease in levels of infrastructure spending, including lower than expected government funding for construction projects; (11) fluctuations in the price of our common stock and inability to complete stock repurchases in the time frame and/or on the terms anticipated; (12) our rates and time utilization being less than anticipated; (13) our inability to manage credit risk adequately or to collect on contracts with customers; (14) our inability to access the capital that our business or growth plans may require; (15) the incurrence of impairment charges; (16) trends in oil and natural gas could adversely affect demand for our services and products; (17) our dependence on distributions from subsidiaries as a result of our holding company structure and the fact that such distributions could be limited by contractual or legal restrictions; (18) an increase in our loss reserves to address business operations or other claims and any claims that exceed our established levels of reserves; (19) the incurrence of additional costs and expenses (including indemnification obligations) in connection with litigation, regulatory or investigatory matters; (20) the outcome or other potential consequences of litigation and other claims and regulatory matters relating to our business, including certain claims that our insurance may not cover; (21) the effect that certain provisions in our charter and certain debt agreements and our significant indebtedness may have of making more difficult or otherwise discouraging, delaying or deterring a takeover or other change of control of us; (22) management turnover and inability to attract and retain key personnel; (23) our costs being more than anticipated and/or the inability to realize expected savings in the amounts or time frames planned; (24) our dependence on key suppliers to obtain equipment and other supplies for our business on acceptable terms; (25) our inability to sell our new or used fleet in the amounts, or at the prices, we expect; (26) competition from existing and new competitors; (27) security breaches, cybersecurity attacks and other significant disruptions in our information technology systems; (28) the costs of complying with environmental, safety and foreign laws and regulations, as well as other risks associated with non-U.S. operations, including currency exchange risk; (29) labor difficulties and labor-based legislation affecting our labor relations and operations generally; (30) increases in our maintenance and replacement costs and/or decreases in the residual value of our equipment; and (31) the effect of changes in tax law, such as the effect of the Tax Cuts and Jobs Act that was enacted on 22 décembre, 2017. For a more complete description of these and other possible risks and uncertainties, please refer to our Annual Report on Form 10-K for the year ended 31 décembre, 2017, as well as to our subsequent filings with the SEC. The forward-looking statements contained herein speak only as of the date hereof, and we make no commitment to update or publicly release any revisions to forward-looking statements in order to reflect new information or subsequent events, circumstances or changes in expectations.

# # #

Personne-ressource :

Ted Grace

(203) 618-7122

Cellulaire : (203) 399-8951

tgrace@ur.com